United States

US equity markets were mixed as earnings season began, with small-cap and value stocks extending their leadership over large-cap and growth shares. The Russell 2000 and S&P MidCap 400 reached new highs, while major large-cap indices eased back from recent record levels. Value stocks outperformed growth for a third consecutive week.

Early earnings results from major banks generated a varied response. Shares in JPMorgan Chase and Citigroup fell after profit declines, while Morgan Stanley and Goldman Sachs advanced on stronger-than-expected results. Sentiment improved later in the week following robust earnings from Taiwan Semiconductor Manufacturing, supporting optimism around artificial intelligence-related investment.

Economic data were broadly supportive. Core inflation slowed further in December to 2.6% year on year, its lowest level since early 2021, while headline inflation edged higher due to energy prices. Retail sales rebounded strongly in November, although growth in GDP-relevant control group sales moderated. Housing data exceeded expectations, supported by lower mortgage rates and easing house price growth, with both new and existing home sales beating forecasts.

In fixed income markets, US Treasuries posted modest gains, with some flattening of the yield curve as the spread between two- and ten-year yields narrowed. Municipal and corporate bonds outperformed amid solid demand, while high-yield markets remained resilient despite weakness in energy-related bonds.

Europe

European equities recorded modest gains, supported by resilient economic data and earnings. The STOXX Europe 600 advanced, although performance across major markets was mixed. Germany and Italy posted gains, France underperformed, and the UK market rose.

Germany emerged from a two-year recession, recording modest growth in the fourth quarter and across 2025 as a whole, driven by stronger domestic demand. Export weakness weighed on activity, reflecting higher US tariffs, a stronger euro, and competition from China, leading to a sharp narrowing of the trade surplus.

The UK economy returned to growth in November, with GDP expanding by 0.3% following two months of contraction. The rebound was driven by services and manufacturing, aided by the reopening of Jaguar Land Rover facilities. The data exceeded expectations and eased near-term growth concerns.

Eurozone industrial production rose for a third consecutive month, while investor sentiment improved to its highest level since mid-2025. Separately, the European Union provisionally endorsed a major free trade agreement with the Mercosur bloc, supporting the region’s longer-term trade outlook.

Japan

Japanese equities rallied strongly, trading near record highs on reports that Prime Minister Sanae Takaichi may call a snap general election. Markets anticipate that a renewed mandate could allow for more aggressive fiscal stimulus, supporting sectors linked to artificial intelligence, defence, and energy.

The yen was volatile but stabilised near JPY 158 per US dollar following verbal intervention from officials. Government bond yields rose as investors priced in higher fiscal spending, while speculation grew that the Bank of Japan could bring forward its next interest rate rise.

China

Mainland Chinese equities declined after regulators tightened margin financing rules, while Hong Kong equities advanced. Despite ongoing property sector weakness and deflationary pressures, recent market gains have been driven by optimism around artificial intelligence and domestic technology firms. China also reported strong export growth in December, recording a record trade surplus for 2025.

Other Key Markets

In Poland, the central bank left interest rates unchanged, citing stable economic growth and easing inflation. South Korea’s central bank also held rates steady, noting improving growth supported by exports - particularly semiconductors - while expecting inflation to gradually converge towards its target

Major Company News:

Carlsberg CEO Jacob Aarup-Andersen says beer remains central despite declining local brand sales, now below 50%. The group is expanding into soft drinks and non-alcoholic options amid growing moderation trends.

Asda faces bond and loan sell-offs as sales plunge 6.5% over Christmas, underperforming its rivals. Investors worry that the UK supermarket’s declining revenue threatens its turnaround under private equity ownership.

WHSmith appoints Leo Quinn as executive chair following an accounting scandal. Investors respond positively, with shares rising 11%, hoping Quinn will restore trust and stabilise the retailer after US profit restatements.

Dunelm shares fall 17% after weak Christmas sales and slowing Black Friday growth. The UK home furnishings group lowers its full-year profit forecast, signalling broader retail challenges over the festive period.

CVC partners with AIG in a $3.5bn deal, deploying insurer capital into private equity, credit, and real estate funds, highlighting growing ties between private markets and insurance investors.

Weekly Update

19th January 2026

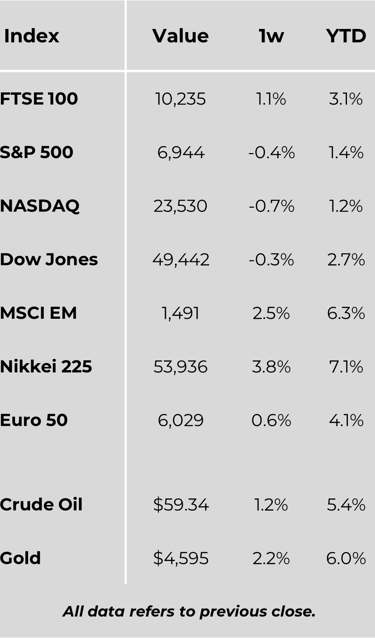

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.