Global markets started the year on a volatile note, as equities and bonds reacted to trade tensions, inflation pressures, and political uncertainty. US stocks swung on tariff headlines, European markets fell amid economic and political developments, and Asian markets were unsettled by Japanese election news and uneven Chinese growth, keeping investors cautious across regions

United States

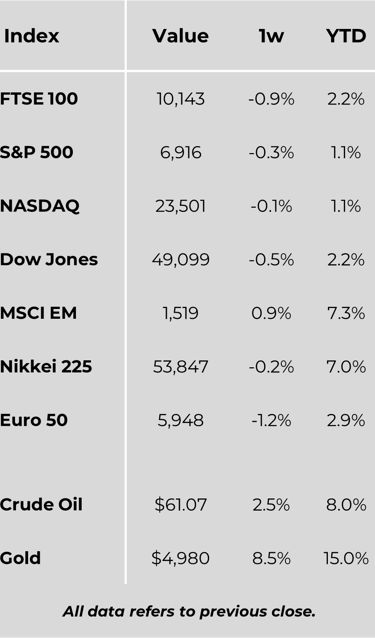

US equity markets ended a volatile, holiday-shortened week lower, as trade tensions and persistent inflation concerns unsettled investors. The S&P MidCap 400 Index was the weakest performer, falling 0.6%, followed by the Dow Jones Industrial Average, which declined 0.5%. The S&P 500 Index slipped 0.4%, while the Russell 2000 lost 0.3%. The Nasdaq Composite was marginally lower over the week. Markets were closed on Monday for Martin Luther King Jr. Day, contributing to sharper midweek moves.

Stocks sold off heavily on Tuesday, with the S&P 500 recording its largest daily decline since October after President Donald Trump announced plans to impose tariffs on European countries opposing US involvement in Greenland. Fears of an escalating global trade dispute weighed heavily on sentiment. However, markets rebounded on Wednesday after Trump signalled a softer approach, citing progress towards a framework agreement with NATO and confirming that the planned tariffs would not proceed. This reversal helped indices finish the week well above their lows.

Economic data remained mixed. Third-quarter GDP growth was revised higher to an annualised 4.4%, up from 4.3%, supported by stronger exports and business investment. Inflation pressures persisted, with core personal consumption expenditures rising 0.2% month on month and 2.8% year on year, still above the Federal Reserve’s target. Labour market conditions remained resilient, as weekly jobless claims stayed near two-year lows, while consumer sentiment improved modestly in January despite ongoing cost-of-living pressures.

In bond markets, US Treasuries posted modest losses amid rate volatility, while corporate bonds outperformed, supported by improving macroeconomic sentiment and steady investor demand.

Europe

European equities declined amid renewed geopolitical and trade uncertainty. The STOXX Europe 600 Index fell 1% in local currency terms. Germany’s DAX dropped 1.6%, France’s CAC 40 lost 1.4%, Italy’s FTSE MIB declined 2.1%, and the UK’s FTSE 100 slipped 0.9%.

Eurozone business activity expanded modestly in January, with the composite PMI holding at 51.5 and business confidence rising to a 20-month high. UK business activity strengthened further, with the composite PMI rising to 53.9. However, official UK data showed continued labour market weakness, slowing wage growth and a surprise rise in inflation to 3.4%. Retail sales volumes increased 0.4% in December, offering some relief for the consumer outlook.

Norway’s central bank kept interest rates unchanged at 4%, while uncertainty increased around the EU–Mercosur trade agreement following a European Parliament vote to seek legal clarification.

Japan

Japanese equity markets fell over the week, with the Nikkei 225 down 0.2% and the TOPIX declining 0.8%. Political uncertainty and concerns over fiscal discipline pushed government bond yields sharply higher after Prime Minister Sanae Takaichi announced an early election and proposed a temporary cut to food consumption taxes. The Bank of Japan left its policy rate unchanged but revised up its growth and inflation forecasts, contributing to volatility in the yen.

China

Chinese markets were mixed. The CSI 300 Index declined 0.6%, while the Shanghai Composite rose 0.8%. Hong Kong’s Hang Seng Index slipped 0.4%. Economic data showed uneven momentum, with solid industrial output offset by weak retail sales and a historic decline in fixed asset investment. While China met its 2025 growth target, concerns remain over the sustainability of growth amid rising global protectionism.

Other Key Markets

In Bulgaria, euro adoption was overshadowed by political upheaval, though analysts expect greater consolidation ahead of snap elections.

In Türkiye, the central bank cut its policy rate by one percentage point to 37% while reiterating its commitment to maintaining a tight monetary stance as inflation risks persist.

Major Company News:

Czech billionaire Daniel Křetínský has launched a takeover bid for Fnac Darty, offering a 19 per cent premium to raise his stake above 50 per cent. Shares jumped, valuing the retailer close to €1.1bn.

Rheinmetall and OHB are in early talks to jointly bid for a military satellite network for Germany’s armed forces, pitched as a Bundeswehr equivalent of Starlink, tapping into Berlin’s €35bn space defence budget.

Private capital group CVC has agreed to buy Marathon Asset Management for up to $1.6bn, boosting fee-paying assets by €17bn. The deal reflects accelerating consolidation across private equity and credit markets.

Ryanair raised forecasts for passenger numbers, fares and profits, citing strong demand and aircraft delivery delays limiting industry capacity. The airline now expects higher pre-tax profits of up to €2.23bn this year.

JD Wetherspoon shares fell after warning profits would dip amid rising costs and tax uncertainty, while rival Young & Co outperformed, reporting stronger sales and planning a move to London’s main market.

Weekly Update

26th January 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.