Global markets were mixed over the week as investors rotated away from high-growth technology shares amid renewed concerns over AI-driven volatility. Value and cyclical stocks outperformed, while weaker US labour data and shifting central bank expectations in Europe added to uncertainty. Japanese equities advanced ahead of elections, whereas Chinese markets slipped despite signs of modest improvement in private-sector activity.

United States

Major US equity indices ended a volatile week mixed. Large-cap technology shares suffered their worst week since November, while small-cap and value-oriented stocks extended their year-to-date gains. Investor unease over the disruptive potential of artificial intelligence, alongside concerns about possible overinvestment in the sector, weighed heavily on high-growth names that have led markets in recent years. By contrast, cyclical and value segments outperformed as investors rotated towards areas with less direct AI exposure. Corporate earnings updates and geopolitical tensions also added to market swings.

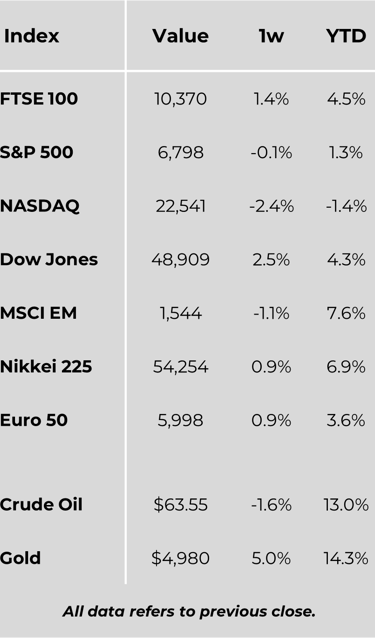

The Nasdaq Composite fell 1.8%, the weakest performer among major indices, while the S&P 500 finished broadly flat. Meanwhile, the Dow Jones Industrial Average, Russell 2000, and S&P MidCap 400 posted solid advances. Value stocks continued to outperform growth, with the Russell 1000 Value Index beating its growth counterpart by more than four percentage points.

Labour market data surprised on the downside. ADP reported private sector payrolls rose by just 22,000 in January, below expectations. Job openings declined to their lowest level since 2020, while layoffs increased. Initial jobless claims also rose, and consulting firm Challenger, Gray & Christmas noted job cuts surged to their highest January level since 2009.

Bond markets were firmer, with Treasury yields falling across most maturities. Investment-grade corporates gained but lagged government bonds, while high yield debt faced some pressure amid softer sentiment.

Europe

European equities advanced, with the STOXX Europe 600 gaining 1%. Germany’s DAX rose 0.7%, France’s CAC 40 climbed 1.8%, and the UK’s FTSE 100 added 1.4%. The ECB kept rates unchanged at 2%, noting resilience in the economy. Inflation slowed faster than forecast, with headline inflation easing to 1.7% and core inflation falling to 2.2%.

Eurozone retail sales dipped in December, though quarterly data suggested improving household demand. The Bank of England also held rates at 3.75%, but a split vote increased expectations of a cut as early as March.

Japan

Japanese equities rose, supported by optimism ahead of the February election. The Nikkei gained 1.8%, while TOPIX climbed 3.7%. The yen weakened to around JPY 157 per dollar amid expectations of fiscal expansion. Household spending fell sharply, highlighting the strain inflation continues to place on consumers.

China

Chinese equities ended lower, with the CSI 300 down 1.3% and the Hang Seng sliding 3%. Private PMI surveys pointed to modest improvement, particularly in services and exports, though official data suggested broader weakness. Markets expect further policy easing this year.

Other Key Markets

In the Czech Republic, the central bank kept rates steady at 3.5%, stressing tight policy remains necessary amid elevated core inflation and property price growth. Poland’s central bank also held rates at 4%, noting inflation may fall back towards target levels in coming quarters.

Major Company News:

UniCredit shares climbed after the Italian bank said it expected to raise its 2025 net profit forecast to €11bn, supported by earnings from its stakes in Commerzbank and Alpha Bank.

Novo Nordisk issued a weak sales and profit outlook last week, sending its shares down nearly 20%. Concerns intensified after US telehealth group Hims & Hers launched a cheaper copycat version of Wegovy, though it later withdrew the product.

Polish parcel locker group InPost is set to be acquired by a consortium led by private equity firm Advent and FedEx in a deal valuing the company at €7.8bn. Following the buyout, Advent and FedEx will each hold a 37% stake, marking a significant move in the European logistics sector.

Big Tech firms are expected to spend heavily on artificial intelligence infrastructure this year, with Alphabet, Amazon and Meta planning vast investments in chips and data centres. Total AI-related capital spending could exceed $660bn, outpacing cash flows even among some of the world’s most profitable companies.

Weekly Update

9th February 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.