Global markets moved higher overall during the week as investors weighed supportive policy developments against mixed economic data and persistent geopolitical risks. US equities gained following a key Supreme Court tariff ruling, while European markets continued to outperform amid improving sentiment. Economic momentum showed signs of moderation across several regions, keeping expectations for central bank policy shifts in focus, with emerging market political developments having limited impact on investor confidence.

United States

US equities ended a holiday-shortened week higher, supported by improving investor sentiment after the US Supreme Court overturned the Trump administration’s broad global tariff regime. Markets were closed on Monday for Presidents’ Day, but stocks gained steadily through the week before rallying sharply on Friday following the ruling. Rising geopolitical tensions between the US and Iran, which pushed oil prices higher, also remained a key focus for investors.

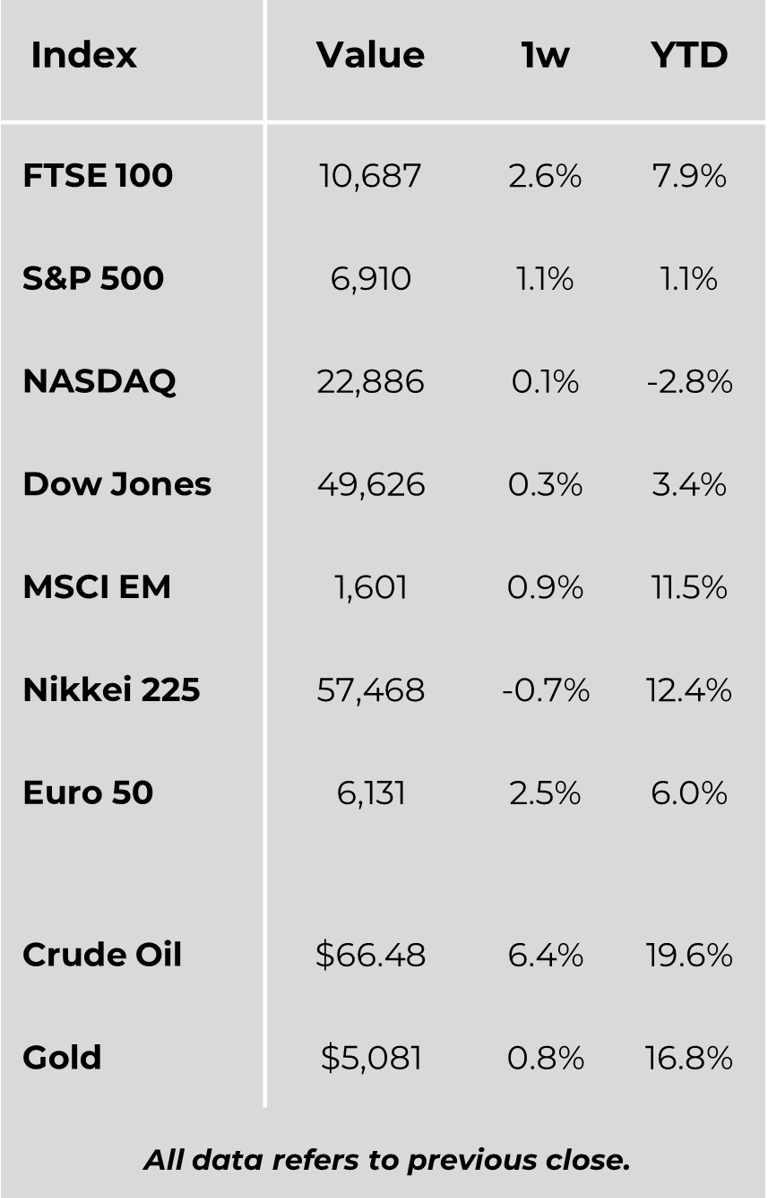

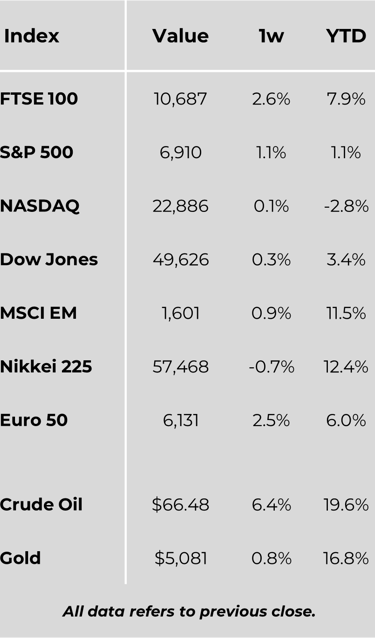

The Nasdaq Composite led major indices, rising 1.5% and recording its first weekly gain since early January. The S&P MidCap 400 and S&P 500 both advanced by more than 1%, while the Dow Jones Industrial Average lagged with a modest 0.3% increase.

Federal Reserve minutes highlighted continued division among policymakers regarding the outlook for interest rates. While some officials favour easing should inflation moderate, others warned that further rate increases may still be necessary if price pressures persist. Supporting this caution, core personal consumption expenditures (PCE) inflation rose 0.4% month on month and 3% year on year in December, signalling renewed inflation momentum.

Economic data pointed to moderating growth. Fourth-quarter GDP expanded at an annualised rate of 1.4%, sharply below the previous quarter’s 4.4% pace, reflecting weaker government spending, exports and consumer demand. Business activity also slowed to a 10-month low in February, although forward-looking expectations improved.

Housing data presented mixed signals, with homebuilder confidence and pending home sales declining amid affordability pressures, while housing starts exceeded expectations. In fixed income markets, US Treasuries posted negative returns as yields rose, while high yield bonds outperformed alongside stronger equity markets.

Europe

European equities continued to outperform, with the STOXX Europe 600 reaching another record high and gaining 2.1% in local currency terms. Strength was driven by improving earnings expectations, supportive macroeconomic data and investor diversification away from technology-heavy US markets. Major indices in Germany, France, Italy and the UK all recorded solid gains, with the FTSE 100 also reaching a new peak.

Eurozone industrial production disappointed, falling more than expected in December, though February PMI data surprised positively as new orders grew at their fastest pace in nearly four years. German investor sentiment eased slightly after January’s strong reading.

In the UK, inflation slowed to 3% year on year in January, while unemployment rose to 5.2% and wage growth moderated. These developments strengthened expectations that the Bank of England could begin cutting rates in coming months.

Japan

Japanese equities declined modestly as geopolitical concerns weighed on risk appetite. Economic growth in the fourth quarter returned to positive territory but fell short of expectations, while consumer inflation slowed to its weakest pace in two years. The yen weakened against the US dollar, and government bond yields declined after reassurances from Prime Minister Sanae Takaichi regarding fiscally responsible policy and targeted investment initiatives.

China

Mainland Chinese markets were largely closed for Lunar New Year holidays, while Hong Kong equities fell slightly upon reopening. The IMF projected China’s economy to grow 4.5% in 2026, emphasising the need to shift towards consumption-led growth supported by structural reforms and stronger policy support.

Authorities also raised VAT on telecommunications services, potentially pressuring sector profitability. Meanwhile, confusion surrounding a briefly updated US list of Chinese firms linked to military activity underscored ongoing geopolitical and trade uncertainties.

Other Key Markets

In Romania, the central bank maintained its benchmark rate at 6.5%, signalling continued caution despite easing inflation. Improved fiscal sentiment followed judicial pension reforms that strengthened confidence in the country’s credit outlook.

In Peru, political instability persisted after Congress removed President José Jeri and installed an interim leader ahead of April elections. Markets reacted calmly, viewing the transition as unlikely to materially alter macroeconomic policy in the near term.

Major Company News:

Schroders’ CEO Richard Oldfield confirmed the company will retain its wealth management arm, Cazenove Capital, following the £9.9bn takeover by Nuveen. He emphasised that Nuveen’s commitments to staff, business and brand apply to the entire group, underlining the strategic importance of the wealth management division.

Novo Nordisk’s once-weekly weight loss injection, CagriSema, fell short in an 84-week trial, achieving 23% weight loss versus 25.5% for rival tirzepatide. Shares dropped 10%, adding to a challenging year marked by board departures, declining stock price, and threats from cheaper copycat versions of its Wegovy treatment.

Rolls-Royce is seeking £100–200mn in initial UK government support for its £3bn UltraFan 30 engine development, key to returning to the short-haul aircraft market. The company aims to secure backing in the first half of the year to fund development and testing of the demonstrator engine.

Johnson Matthey agreed to sell its catalyst technologies business to Honeywell for £1.3bn, down from £1.8bn agreed last year. Shares fell 15% despite a strong 50% rise over the past year, reflecting the price reduction in its key unit sale and investor disappointment.

Weekly Update

23rd February 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.