Global markets experienced a mixed week as investors navigated a combination of technological disruption, geopolitical tensions, and economic data releases. In the US, concerns about artificial intelligence (AI) and trade uncertainties weighed on equities, while Treasury yields fell amid risk aversion. Europe benefited from strong corporate earnings, although regional inflation data remained uneven. Asian markets were buoyed by policy optimism and domestic stimulus measures, while emerging markets faced political and election-driven volatility. Commodities reacted sharply to escalating Middle East tensions.

United States

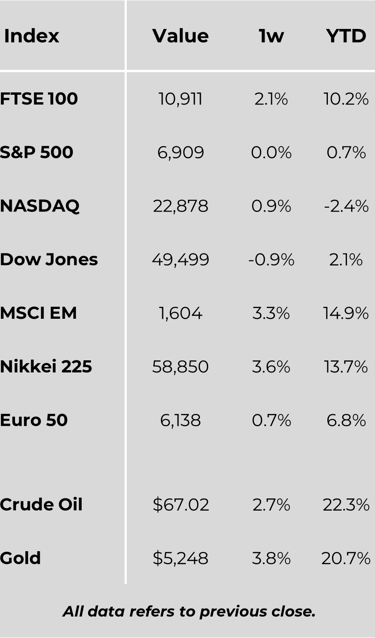

Major US stock indexes fell, with the Dow Jones Industrial Average declining 1.31% and the S&P 500 losing 0.44%, as investors weighed AI-driven disruption and global trade concerns. Equities dipped early in the week before modest gains around NVIDIA’s strong earnings were unable to reverse broader losses. Economic data painted a mixed picture: producer prices rose 0.5% month-over-month in January, surpassing expectations, while factory orders fell 0.7% in December due to weaker aircraft bookings. Consumer confidence inched higher to 91.2, but remained well below its November 2024 peak. Weekly jobless claims rose slightly to 212,000, though continuing claims fell to 1.833 million. US Treasuries benefitted from the risk-off tone, pushing 10-year yields below 4% for the first time since November, while investment-grade corporate bonds posted modest gains and high-yield performance was mixed.

Europe

European equities were supported by robust earnings and diversification away from the tech-heavy US market. The STOXX Europe 600 rose 0.52%, with Germany’s DAX, Italy’s FTSE MIB, and France’s CAC 40 all posting gains. The UK’s FTSE 100 climbed 2.06% to a new high midweek. Business confidence improved in Germany, while France saw a slight dip. Inflation trends were mixed: February readings showed modest increases in France and Spain, but eased in Germany. In the UK, Bank of England officials signalled potential rate cuts in 2026, and trade concerns eased following US reassurances.

Japan

Japanese equities rallied, with the Nikkei 225 up 3.56% and TOPIX 3.42%, reaching record highs. Investors responded positively to policy signals from Prime Minister Sanae Takaichi and a cautious Bank of Japan stance. The yen weakened to JPY 156 against the dollar, while the Tokyo-area CPI rose 1.8% year-over-year.

China

In China, mainland markets advanced as Lunar New Year activity boosted tourism, while Shanghai eased homebuying restrictions and the central bank took measures to slow yuan appreciation.

Other Key Markets

Hungary cut its key rate to 6.25%, balancing easing with election uncertainties, while Colombia faced renewed market volatility amid shifting election polls, strengthening support for left-wing policies and prompting currency and bond weakness.

Commodities

Oil and gas prices surged following Middle East attacks, with European gas up 24%. Gold rose 2.2% to $5,390 per troy ounce as investors sought safe havens, while global equities sold off amid heightened geopolitical risk.

Major Company News:

QatarEnergy, a leading LNG supplier, announced production halts at Ras Laffan and Mesaieed following drone attacks from Iran. Shipments through the Strait of Hormuz have stopped, affecting global supply, particularly China, which sources around a quarter of its LNG from Qatar.

Defence stocks surged as investors anticipated higher weapons demand amid Middle East tensions, with Lockheed Martin, Northrop Grumman, and Raytheon owner RTX all rising over 5%. European defence firms also gained, while US airlines and luxury stocks, including United, American Airlines, Kering, and LVMH, fell on inflation and conflict concerns.

Toyota raised its offer to privatise Toyota Industries to ¥5.9tn ($37.8bn), up 9.6%, following pressure from activist investor Elliott Management. The move comes after Elliott criticised the initial bid as undervaluing the company and successfully urged shareholders not to tender, prompting Toyota to sweeten the deal ahead of the tender deadline.

BYD’s February sales plunged 41% year-on-year to 190,190 units, marking its largest decline in five years. Domestic sales fell 65%, and export growth of 50% was insufficient to offset the slowdown, highlighting the challenges the EV giant faces as it pivots toward international markets amid weakening home demand.

TalkTalk is set to receive an additional £115mn from shareholders and lenders, including £65mn in senior debt and a £50mn short-term facility. The funding aims to strengthen the UK broadband provider’s finances as potential buyers consider acquiring parts of the business, supporting its operations amid heavy indebtedness.

Weekly Update

2nd March 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.