Markets were dominated by heightened geopolitical risk as US-Israeli strikes in Iran and subsequent retaliatory actions raised concerns over energy supply and inflation. Crude oil and gas prices surged on the prospect of disruption to flows through the Strait of Hormuz, injecting a geopolitical premium into energy markets. Investors sought safe havens, driving up US Treasury and gold prices, while equity markets saw broad volatility. The conflict, combined with rising energy costs, weighed on sentiment globally, with markets closely monitoring its duration and potential economic repercussions.

United States

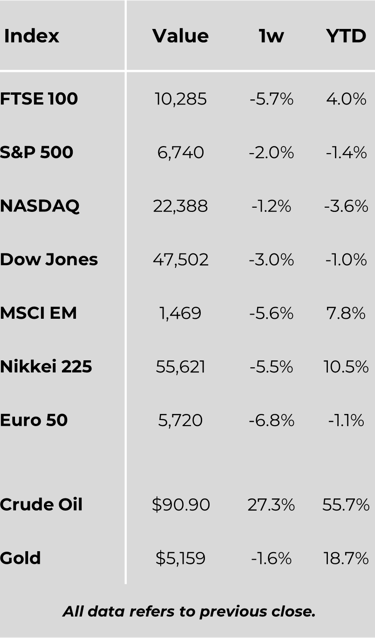

Major US indexes ended the week lower, with the S&P MidCap 400 falling 4.6% and the Nasdaq Composite down 1.2%. Oil-driven inflation concerns, mixed economic data, and uncertainty over Federal Reserve policy drove volatility. February ISM data pointed to ongoing economic expansion, with the manufacturing PMI at 52.4 and the services PMI at 56.1, the latter its highest since July 2022. Employment data were mixed: ADP reported a rise of 63,000 private sector jobs, while nonfarm payrolls declined by 92,000, raising questions over labour market strength and the Fed’s next moves.

Europe

The STOXX Europe 600 Index fell 5.6% amid deteriorating risk appetite. Germany’s DAX dropped 6.7%, Italy’s FTSE MIB 6.5%, France’s CAC 40 6.8%, and the UK’s FTSE 100 5.7%. Rising energy prices and higher inflation expectations pressured markets. Eurozone inflation rose to 1.9% in February, while unemployment unexpectedly fell to 6.1%. Italy’s GDP expanded 0.3% in Q4 2025, and unemployment fell to 5.1%. In the UK, the Construction PMI declined, but house prices rose 1.3% year-on-year.

Japan

Japanese equities were sharply lower, with the Nikkei 225 down 5.5% and the TOPIX 5.6%, amid uncertainty over the Middle East conflict and higher crude oil costs. The yen weakened to JPY 157.6 against the dollar, prompting officials to consider intervention. BoJ Governor Kazuo Ueda signalled readiness to adjust rates in line with economic and price developments, while wage negotiations could influence domestic consumption.

China

Chinese markets retreated, with the CSI 300 down 1.1% and the Hang Seng 3.3%, as investors balanced Middle East risks against Beijing’s moderated growth targets. China set a 2026 GDP target of 4.5–5%, highlighting domestic demand, investment, and technology self-sufficiency. February manufacturing data were mixed, with the official PMI in contraction at 49.0, while private surveys suggested expansion.

Middle East

The US-Israeli strikes and Iranian retaliation elevated regional geopolitical risk. Markets reacted with higher oil prices, increased energy equities, and volatility across global markets. The focus remains on energy supply continuity and the conflict’s duration, with longer-term implications for inflation, growth, and financial market stability still uncertain.

Major Company News:

Assured Guaranty has refused to insure UK water utilities’ financing for over a year, amid debt concerns, despite $15bn exposure and repeated requests from companies since Thames Water’s default.

Telefónica may pursue further UK broadband acquisitions to expand Virgin Media O2, challenging BT’s Openreach, following its £2bn Netomnia deal and focus on fibre network growth in key markets.

Nvidia-backed UK AI cloud start-up Nscale raised $2bn, valuing the two-year-old company at $14.6bn, with Meta veterans Sheryl Sandberg and Nick Clegg joining the board, supporting European cloud expansion.

Creditors of bankrupt car parts maker First Brands expect less than $200mn from asset sales, risking heavy losses on $12bn of debt, as advisers seek buyers for several units in coming weeks.

Weekly Update

9th March 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.