Global financial markets faced a more unsettled week as geopolitical tensions in the Middle East intensified, leading to sharp movements in energy prices. Concerns about possible disruptions to oil supplies through the Strait of Hormuz - a key route for global energy shipments - prompted periods of volatility across equities, bonds and commodities. Although occasional signs of diplomatic de-escalation provided some relief, the overall tone remained cautious as investors weighed the potential economic consequences of higher energy prices.

United States

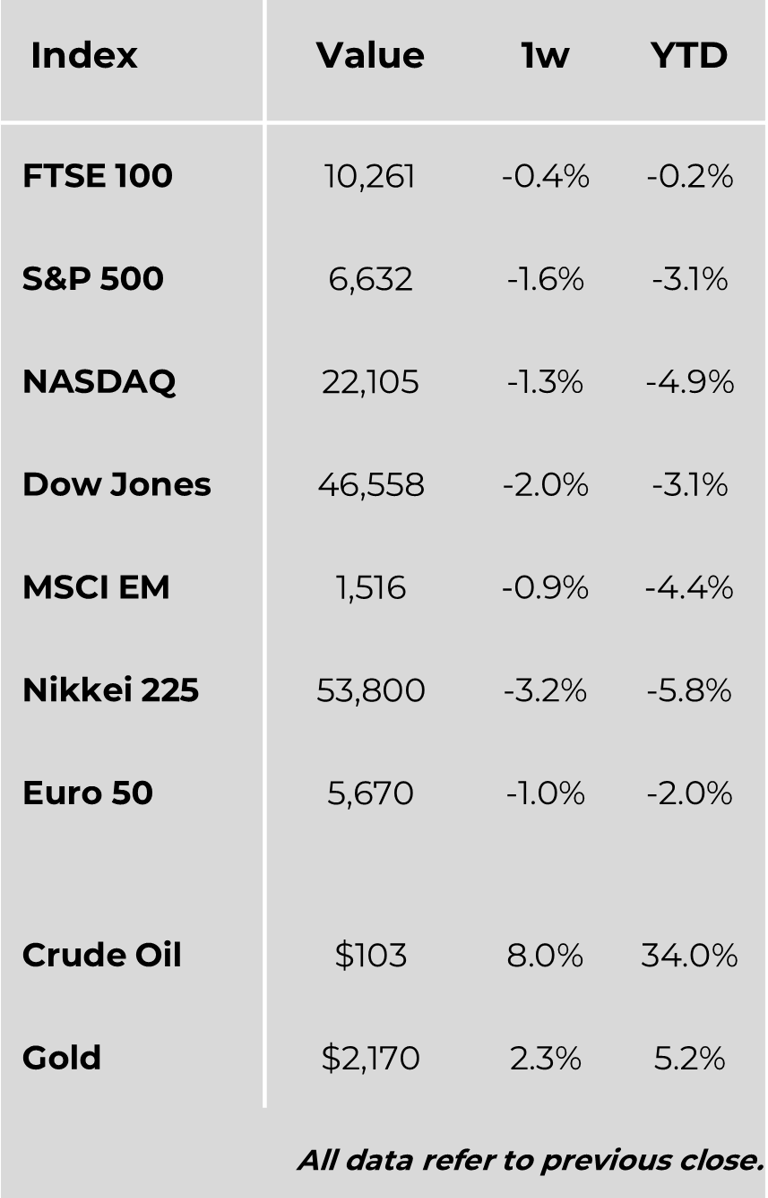

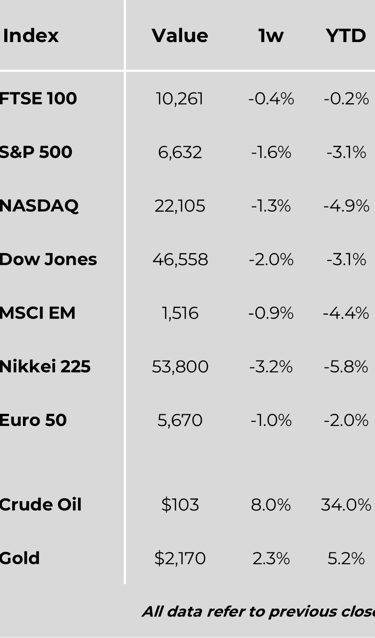

US equity markets declined for a third consecutive week, reflecting a more risk-averse mood among investors. Mid-cap stocks and the Dow Jones Industrial Average led the losses, while technology shares proved somewhat more resilient. Rising oil prices, ongoing trade policy developments and signs of stress in private credit markets all contributed to the cautious sentiment.

Economic data painted a mixed picture. Inflation remains relatively persistent, with the Federal Reserve’s preferred measure rising modestly and reaching its highest level since early 2024. At the same time, economic growth in the final quarter of last year was revised lower, suggesting that momentum may be easing. Some areas of the economy, however, remain supportive. The housing market showed tentative improvement, with existing home sales rising and affordability gradually improving, although activity remains below pre-pandemic levels.

Europe

European equities also edged lower during the week as investors monitored developments in energy markets and their potential impact on regional growth. Germany’s DAX index declined modestly, while France’s CAC 40 experienced slightly larger losses. Italy was one of the few major markets to register a gain.

Economic indicators were generally weak. German factory orders and exports both declined sharply, while industrial production across the eurozone fell more than expected. Policymakers remain alert to the inflationary implications of higher energy prices, though officials have suggested the region is better positioned to cope with energy shocks than in previous years.

United Kingdom

In the UK, the FTSE 100 finished the week slightly lower. Economic data highlighted the fragile state of domestic growth, with official figures showing that the economy stagnated in January after only marginal expansion at the end of last year. The services sector - the largest component of the UK economy - showed little overall growth during the month.

Japan

Japanese equities weakened as investors assessed the potential economic impact of higher oil prices. The country’s heavy reliance on imported energy leaves it particularly exposed to supply disruptions in the Middle East. In response, the government announced plans to release part of its strategic oil reserves and introduce measures aimed at limiting increases in domestic fuel prices.

Meanwhile, Japanese government bond yields rose modestly, partly reflecting a weaker yen and concerns that higher energy costs could feed through into inflation.

Asia

Markets across Asia produced mixed results. Chinese equities showed only modest movement overall, with gains in some mainland indices offset by declines in Hong Kong. Economic data suggested stronger consumer inflation, supported by seasonal spending, while export growth proved robust - particularly in technology-related sectors benefiting from strong global demand.

Commodities

Commodity markets were dominated by developments in energy. Oil prices surged at the start of the week amid fears that disruptions around the Strait of Hormuz could affect global supply, briefly pushing Brent crude close to $120 per barrel before easing slightly. The International Energy Agency coordinated a large release of strategic reserves in an effort to stabilise markets.

Higher oil prices also lifted a range of related commodities, including biofuel feedstocks and certain industrial materials, reflecting broader concerns about supply chains and inflation.

Major Company News:

Meta is reportedly preparing significant job cuts that could affect around 20% of its workforce as rising spending on artificial intelligence infrastructure pressures profitability across large technology firms.

Mercedes-Benz is holding early discussions with Chinese automaker Geely about expanding their partnership, potentially deepening cooperation in areas such as electric vehicles and technology development.

Creditors of Thames Water have proposed a £3.35 billion equity injection alongside new debt financing as part of a restructuring plan aimed at stabilising Britain’s largest water utility.

Foxconn forecast strong revenue growth this year despite reporting weaker-than-expected profits, highlighting continued demand for electronics manufacturing linked to global technology and AI supply chains.

French energy group TotalEnergies plans to begin the second phase of production at Azerbaijan’s Absheron gas field by 2029, expanding output from the Caspian Sea project

Weekly Update

16th March 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.