Global markets experienced another unsettled week as geopolitical tensions in the Middle East continued to dominate sentiment. Disruptions to shipping routes through the Strait of Hormuz heightened concerns about global energy supplies, pushing oil and gas prices higher and adding to inflation worries. Central bank decisions and mixed economic data further contributed to market volatility, leaving investors cautious as they assessed the potential economic impact of sustained energy price pressures.

United States

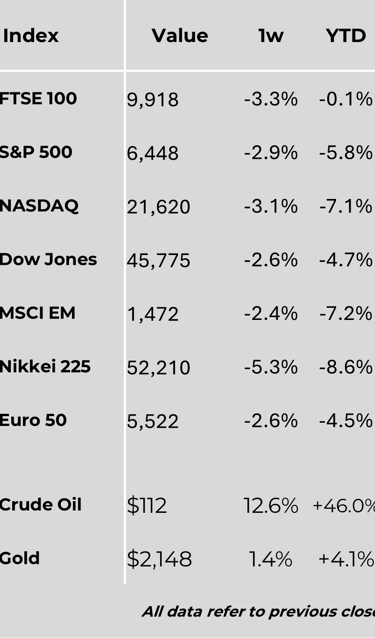

US equity markets ended the week lower following heightened volatility driven by rising oil prices, inflation concerns and cautious signals from the Federal Reserve. The Dow Jones Industrial Average recorded the largest decline, with technology-heavy indices also moving lower. The energy sector proved a notable exception, benefiting from higher crude prices amid continued uncertainty surrounding Middle East supply risks.

The Federal Reserve left interest rates unchanged at its latest meeting, maintaining the current policy range for a second consecutive month. Policymakers indicated that only one further rate cut may be delivered this year, while forecasts for both inflation and economic growth were revised slightly higher. Federal Reserve Chair Jerome Powell highlighted geopolitical developments as a key source of uncertainty, particularly the risk that higher energy prices could feed into inflation expectations.

Recent economic data added to these concerns. Producer prices rose more quickly than expected, suggesting persistent inflationary pressure within supply chains. Housing data provided a mixed picture: pending home sales and builder sentiment improved modestly, but new home sales fell to their lowest level since 2022, underlining the continued affordability challenges facing buyers.

Europe

European markets also moved lower as investors monitored developments in global energy markets. Major indices across Germany, France and Italy recorded declines, reflecting the region’s sensitivity to energy price shocks. Central banks across the region, including the European Central Bank, opted to keep interest rates unchanged but warned that sustained increases in oil and gas prices could place renewed upward pressure on inflation.

Economic indicators remained mixed. The eurozone recorded a widening trade deficit, largely driven by weaker exports in key industrial sectors such as machinery and chemicals. In Germany, producer prices declined year on year, reflecting earlier falls in energy costs, though the outlook remains uncertain as global fuel prices rise.

United Kingdom

UK markets followed global trends, with the FTSE 100 ending the week lower. The Bank of England kept its key interest rate unchanged but warned that prolonged energy price increases could reignite inflationary pressures and potentially delay any further easing in monetary policy.

Business sentiment also showed signs of strain. Survey data indicated that UK manufacturers are facing weakening domestic demand alongside rising cost pressures, reinforcing concerns that economic growth may remain subdued in the near term.

Japan

Japanese markets weakened slightly during the week as investors assessed the potential impact of higher energy costs on the country’s import-dependent economy. The Bank of Japan kept interest rates unchanged, although policymakers signalled that further gradual tightening remains possible if inflation pressures persist.

The Japanese yen strengthened modestly but remains weak by historical standards, supporting exporters while increasing the cost of imported goods. Export data showed continued growth overall, though shipments to the United States and China softened, highlighting uneven global demand.

Asia

Markets across Asia delivered mixed performance. Chinese equities moved lower as investors weighed the impact of rising global energy costs alongside ongoing concerns about domestic demand. Recent economic data offered modest encouragement, with industrial production and retail sales exceeding expectations and signs emerging of tentative stabilisation in the property market.

Trade tensions also returned to focus, with the possibility of new US tariffs on major trading partners creating additional uncertainty for the region’s export outlook.

Commodities

Commodity markets remained firmly in the spotlight. Oil prices climbed further amid continuing disruptions to shipping routes through the Strait of Hormuz, reinforcing fears of prolonged supply shortages. Natural gas markets also tightened following damage to major export infrastructure in the Gulf region, pushing prices higher across Europe and Asia.

These developments underline the sensitivity of global markets to geopolitical risk. With energy costs rising and inflation concerns lingering, investors are likely to remain focused on geopolitical developments and central bank responses in the weeks ahead.

Major Company News:

Airbus has agreed to acquire Ultra Cyber from Cobham Ultra, strengthening its cybersecurity capabilities and expanding its UK-based defence technology footprint as demand for secure digital infrastructure continues to grow.

Unilever is reportedly in discussions to sell parts of its foods division to US spices group McCormick, in a move that could streamline its portfolio and sharpen focus on higher-growth brands.

London Stock Exchange Group has announced leadership changes within its European equities division, aiming to strengthen its competitive position and support new product development across regional trading platforms.

FedEx shares rose sharply after the logistics group reported stronger-than-expected earnings and raised its fiscal outlook, signalling resilient parcel demand despite rising geopolitical and economic uncertainty.

Bavarian Nordic has continued its share buyback programme, reflecting confidence in its balance sheet and ongoing investment strategy within the European vaccines and biotechnology sector.

Weekly Update

23rd March 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.