Global markets were driven by geopolitical tensions and rising energy prices, fuelling volatility and inflation concerns. US equities remained under pressure, while Europe showed modest resilience despite weakening growth signals. Across Asia, policy responses to energy shocks intensified, and China faced renewed trade tensions and equity declines, highlighting a fragile and uncertain global economic backdrop.

United States

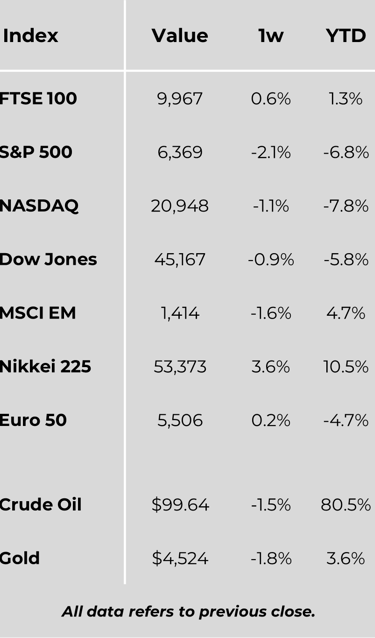

US equity markets experienced a volatile, headline-driven week as investors reacted to developments in the Middle East, fluctuating oil prices, and continued pressure on large-cap technology stocks. While mid- and small-cap indices, including the S&P MidCap 400 and Russell 2000, rebounded after four weeks of losses, the S&P 500, Dow Jones Industrial Average, and Nasdaq posted their fifth consecutive weekly declines. Value stocks outperformed growth for a third straight week, reflecting investors’ preference for defensive positioning.

Economic data showed moderation in business activity, with the Flash Composite PMI falling to an 11-month low of 51.4, driven by weaker services output. Inflationary pressures rose, particularly in energy-sensitive sectors, while employment contracted slightly, signalling cautious corporate spending. Jobless claims were largely stable, though consumer sentiment declined to a 53.3 reading, highlighting concerns about short-term economic prospects and higher expected inflation. US Treasuries ended the week near unchanged, reflecting elevated geopolitical risk and the possibility of a Federal Reserve rate adjustment, while high-yield bonds saw mixed trading amid M&A activity and shifting sentiment.

Europe

European markets advanced modestly, with the STOXX Europe 600 up 0.35%, though performance varied regionally. Italy and France outperformed, while Germany lagged, reflecting soft business confidence amid rising energy costs and Middle East uncertainties. The ECB signalled readiness to adjust rates if necessary but emphasised patience, while the OECD revised down growth forecasts for the eurozone and UK due to geopolitical pressures. Eurozone PMI readings showed slowing activity and contracting new orders, suggesting supply chain disruptions and heightened caution among businesses. The UK reported steady inflation at 3%, though energy-related price pressures are likely to weigh going forward.

Japan

In Japan, equities were mixed as higher oil prices and Middle East tensions weighed on sentiment. The yen remained weak near intervention levels, prompting verbal warnings from authorities. The 10-year JGB yield rose to 2.34%, reflecting global yield pressures and expectations for gradual BoJ policy normalisation. Core inflation eased slightly, aided by government subsidies, but elevated energy costs continue to pose upside risk.

China

Chinese equities declined as investors weighed higher oil prices against ongoing earnings pressure. Domestic fuel prices were capped to limit inflation pass-through, while industrial profits grew sharply in early 2026. Trade tensions with the US escalated through six-month investigations, though Beijing signalled a softer stance on trade balance and foreign investment.

Asia

Across Asia, energy price shocks prompted swift policy responses. The Philippines declared an energy emergency, Thailand and Malaysia raised fuel prices, and South Korea implemented bond buybacks to stabilise markets. India and Indonesia combined targeted measures with fiscal support to manage inflation and market volatility.

Major Company News:

TotalEnergies capitalised on Middle East supply disruptions in March, purchasing 70 crude oil cargoes from the UAE and Oman—more than double February’s volume—generating over $1bn in trader profits amid wartime market volatility.

Emirates is paying just $100,000 per week for “war risk” insurance on its fleet amid the US-Israel conflict with Iran, far lower than the $70,000–$150,000 per flight charged to other airlines operating in the Middle East.

Apple’s Irish subsidiary, Apple Distribution International (ADI), was fined £390,000 by the UK’s OFSI for 2022 payments of £635,618.75 to Russian streaming service Okko, breaching sanctions; ADI manages Apple product sales and App Store payments across Europe and the Middle East.

French AI start-up Mistral raised $830m in its debut debt financing to build Nvidia-powered data centres across Europe, supporting its €4bn AI infrastructure plan amid rising demand for European “sovereign” alternatives to US tech giants.

US pharma giant Eli Lilly struck a $2bn deal with Hong Kong-listed AI biotech Insilico Medicine, securing exclusive rights to a GLP-1 diabetes drug, reflecting growing global reliance on China-based drug discovery and development partnerships.

Weekly Update

30th March 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.