Global markets delivered broadly positive performance over the week, despite ongoing geopolitical tensions in the Middle East and heightened energy price volatility. Investor sentiment improved on tentative signs of de-escalation, supporting equities, while bond yields generally declined. Uncertainty around inflation, central bank policy, and energy costs, however, continues to shape the near-term outlook across regions.

United States

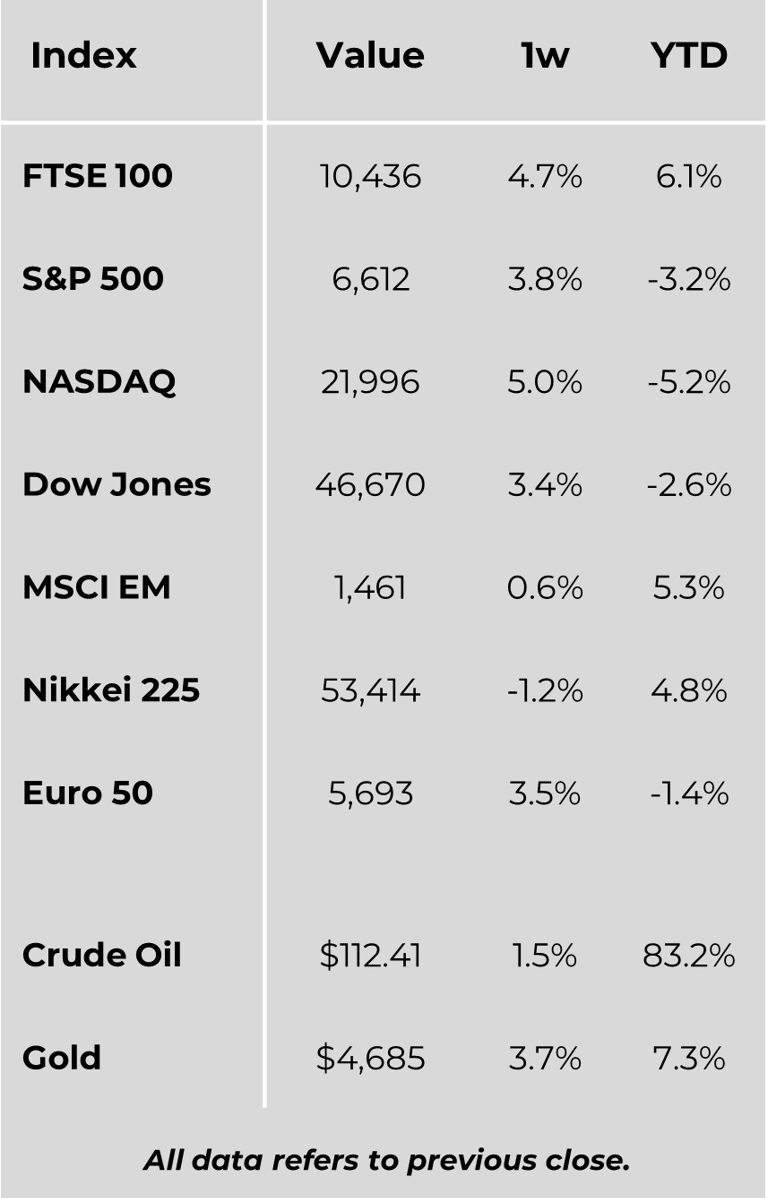

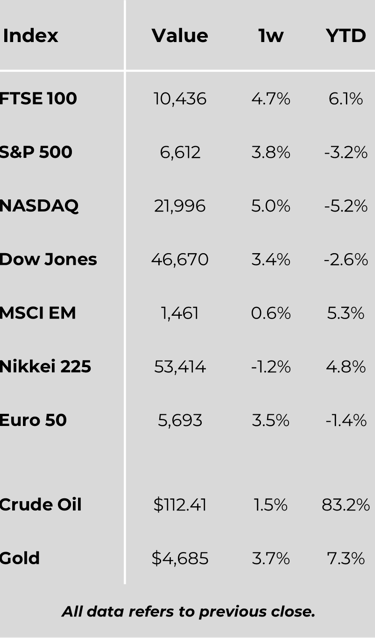

Major US equity indices ended a volatile, holiday-shortened week higher, supported by tentative signs of de-escalation in the Middle East. The Nasdaq Composite led gains, recording its strongest weekly performance since November, while the S&P 500 and Dow Jones Industrial Average rose 3.36% and 2.96%, respectively. Smaller-cap stocks also advanced.

Markets initially weakened but rallied midweek as signals emerged that US military involvement in Iran might ease. Sentiment turned cautious after a lack of clarity on timelines, pushing oil prices higher before equities recovered into Thursday’s close.

US Treasury yields declined, with the 10-year yield falling to around 4.31%, supported by softer inflation concerns following remarks from Federal Reserve Chair Jerome Powell.

Economic data were mixed. Job creation modestly exceeded expectations, and jobless claims improved, though continuing claims rose. Job openings declined, indicating softer labour demand. Consumer confidence edged higher for a second consecutive month, while manufacturing activity expanded, albeit with ongoing weakness in employment and rising price pressures.

Europe

European equities posted strong gains, with the STOXX Europe 600 up 3.92%. Markets were buoyed by hopes that geopolitical tensions may prove short-lived. Major indices across Germany, France, Italy, and the UK all advanced.

Eurozone inflation rose to 2.5% in March, driven primarily by higher energy costs, while other components moderated. Germany’s growth outlook was revised sharply lower due to the energy shock.

Regional data were mixed: Spain’s manufacturing sector contracted, while Sweden’s showed robust expansion. Swiss retail sales remained positive. In the UK, manufacturing growth softened slightly, although forward indicators improved, and house price growth accelerated.

Japan

Japanese equities declined, reflecting sensitivity to rising oil prices and geopolitical risks. The Nikkei 225 fell 1.7%.

Expectations grew that the Bank of Japan may raise rates amid inflation concerns linked to energy costs. Bond yields rose, while the yen strengthened modestly on speculation of potential currency intervention.

Economic data were weaker overall, with softer inflation, declining industrial production, and a sharper-than-expected fall in retail sales.

China

Chinese markets were mixed, balancing improving domestic data against external uncertainties. PMI readings indicated a broad-based recovery across manufacturing and services, supporting near-term stabilisation, though rising input costs remain a concern.

China also moved to remove export tax rebates on key clean energy products, signalling efforts to address overcapacity but increasing cost pressures.

Other Key Markets

In Colombia, political tensions surrounding the central bank introduced policy uncertainty despite a rate rise, raising concerns about institutional independence.

In India, the central bank intensified efforts to support the currency, tightening foreign exchange rules. This triggered volatility across markets, with the rupee stabilising but equities—particularly financials—coming under pressure.

Major Company News:

JPMorgan Chase has secured approval to construct a 265-metre tower in Canary Wharf, set to become the area’s tallest building. An agreement with London City Airport resolved height concerns, allowing the new UK headquarters to surpass One Canada Square.

Shares in major US health insurers surged after the Trump administration approved a 2.5% increase in Medicare payments, equating to over $13bn by 2027. Stocks of Humana and UnitedHealth rose sharply, reflecting improved earnings expectations.

Bill Ackman’s Pershing Square Capital has proposed acquiring Universal Music Group in a €55bn deal via a SPAC merger, potentially shifting its listing to New York. Shares jumped after the offer, despite recent declines linked to concerns over AI’s impact on music industry profitability.

A data centre project backed by Meta is seeking $3bn in construction loans for an off-grid campus powered by on-site natural gas. The deal structure is novel, with lenders financing both infrastructure and energy assets in a single transaction, marking a first for large-scale data centre developments.

Amazon is in talks to acquire satellite operator Globalstar, aiming to strengthen its low Earth orbit ambitions. Negotiations are ongoing, with Apple’s 20% stake adding complexity and requiring parallel discussions between the parties.

Weekly Update

7th April 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.