Global markets rallied strongly over the week as geopolitical tensions in the Middle East eased following reports of a US - Iran ceasefire framework. The resulting decline in oil prices supported a broad risk-on move across equities, credit, and currencies. Equities rose across all major regions, led by technology and cyclical sectors, while inflation dynamics and growth concerns continued to shape the broader macroeconomic backdrop.

United States

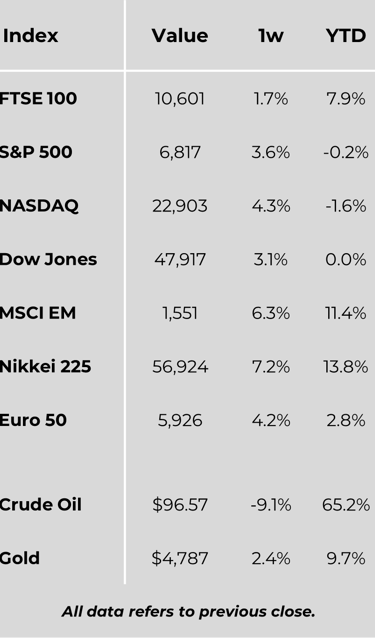

US equities extended gains for a second consecutive week, with major indices rising over 3%. The Nasdaq Composite outperformed, climbing 4.68%, driven by continued strength in artificial intelligence-linked stocks and large-cap technology names. Investor sentiment was supported by optimism around sustained AI infrastructure investment and semiconductor demand.

Within the S&P 500, energy was the only sector to decline, reflecting the sharp drop in oil prices, while information technology, consumer discretionary, and communication services led gains. US Treasuries also delivered positive returns, indicating a modest easing in risk aversion.

On the macroeconomic front, inflation accelerated, with headline CPI rising to 3.3% year on year, largely driven by higher energy costs. Core inflation remained comparatively contained. However, consumer sentiment deteriorated notably, reflecting growing concerns over persistent price pressures and weaker asset values, even as services activity remained in expansion territory.

Europe

European equities posted solid gains, with the STOXX Europe 600 rising just over 3% in local currency terms. Markets were buoyed by improving global risk sentiment and expectations of reduced geopolitical disruption.

Despite the equity rally, the macroeconomic backdrop remained more cautious. The European Commission signalled potential downward revisions to growth forecasts, citing risks of a stagflationary environment characterised by weak growth and elevated inflation. Activity data was mixed, with services sectors in France and Italy contracting, while broader demand conditions remained subdued. In the UK, house price growth remained modest and below expectations, pointing to ongoing softness in the housing market.

Japan

Japanese equities rebounded strongly, with the Nikkei 225 rising 7.15% and the TOPIX gaining 2.6%, as exporters and technology stocks benefited from improved risk appetite and lower oil prices. The rally reflected relief over easing geopolitical tensions, which reduced concerns around energy supply disruptions.

However, inflationary pressures remained evident. Producer price inflation accelerated to 2.6% year on year, driven largely by higher energy costs. Consumer sentiment weakened, highlighting growing household pressure from rising prices. Government bond yields continued to climb towards multi-decade highs, with markets increasingly pricing in the possibility of tighter monetary policy from the Bank of Japan.

China

Chinese equities ended the week higher, supported by easing geopolitical tensions and improving sentiment around global trade and energy markets. The CSI 300, Shanghai Composite, and Hang Seng Index all posted solid gains.

Producer price inflation turned positive for the first time in over three years, reflecting rising commodity and energy costs rather than broad-based demand strength. Consumer inflation remained subdued. Meanwhile, regulatory tightening in equity markets, including new restrictions on short-term trading by major shareholders, signalled continued policy focus on market stability.

Major Company News:

Goldman Sachs reported $5.6bn quarterly net income, its highest in five years, driven by record equities trading performance that offset weaker fixed-income revenues, beating analyst expectations.

Volkswagen, Renault and BMW are considering range-extended electric vehicles, a hybrid-style technology using small engines as generators, as they seek to compete with Chinese EV makers while easing full-electrification transition risks.

JAB Holdings booked a $6bn gain in 2025 from selling its JDE Peet’s stake, offsetting heavy losses at Coty and Krispy Kreme, highlighting mixed performance across its consumer portfolio.

Perella Weinberg Partners is acquiring UK boutique advisory firm Gleacher Shacklock in a cash-and-stock deal, as US mid-sized investment banks expand their European advisory footprint beyond the bulge bracket.

Sotheby’s is offering sellers 7% interest to delay receiving sale proceeds via extended settlement terms, as weak art market conditions strain auction house liquidity.

Weekly Update

13th April 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.