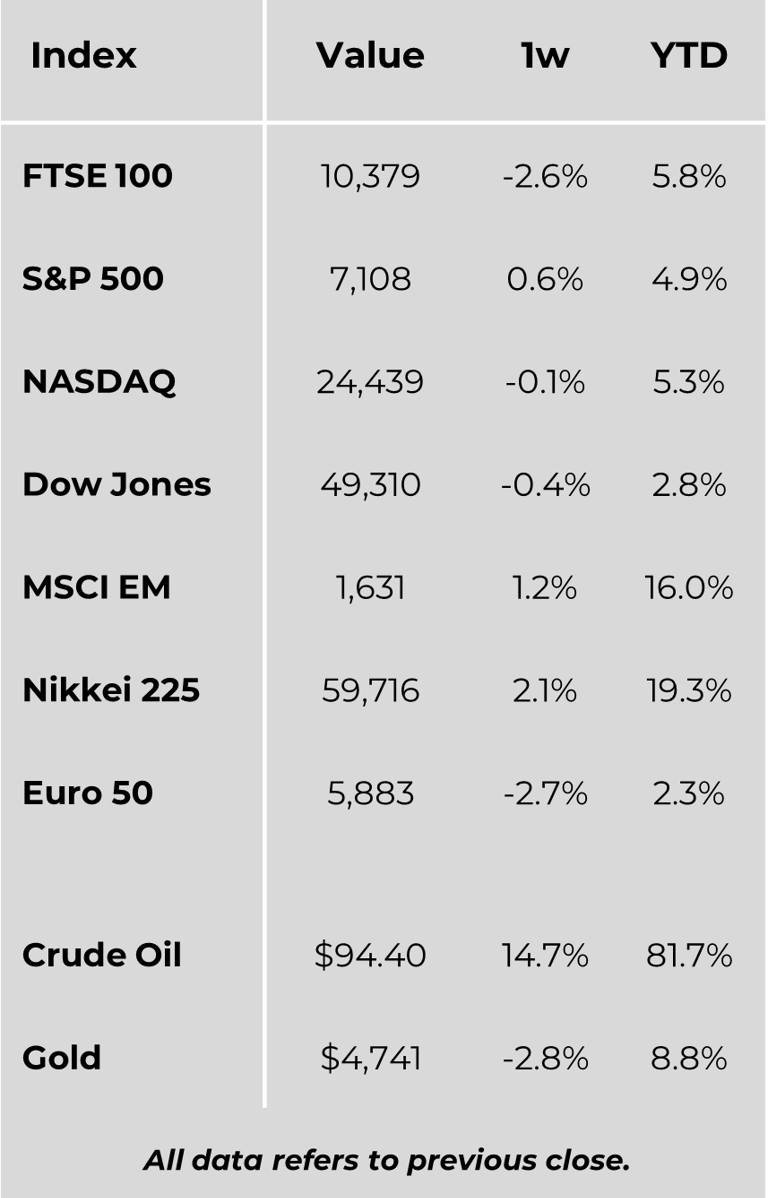

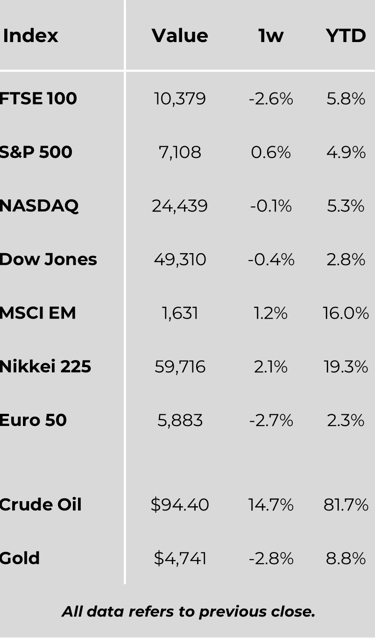

Global equity markets delivered a mixed performance over the week, with US stocks advancing to fresh highs on AI-driven strength and resilient earnings, despite lingering geopolitical uncertainty. Europe lagged as sentiment deteriorated on weaker confidence data and elevated energy-related risks. Japan saw split performance, with tech strength offset by broader weakness and rising inflation pressures. China remained stable, supported by steady policy settings and solid growth momentum. Across markets, inflation concerns, geopolitical tensions, and central bank caution remained dominant themes.

United States

US equities ended the week on a mixed but broadly firmer footing, with most major indices advancing and several touching record highs. Gains were led by the Nasdaq Composite, supported by continued momentum in artificial intelligence (AI)-related stocks, followed by the S&P 500 and Russell 2000, while the Dow Jones Industrial Average lagged. Markets were initially cautious after a strong rally in prior weeks, as optimism over a near-term de-escalation in the Middle East faded. Sentiment improved midweek following an extension of the ceasefire, although geopolitical uncertainty remained a persistent overhang.

Corporate earnings were a key focal point, with roughly one-fifth of S&P 500 constituents reporting. Results were generally robust, with a strong majority exceeding expectations and overall earnings growth remaining firmly in double-digit territory. Investors continued to monitor AI-driven demand, consumer resilience, and corporate cost management.

Economic data painted a mixed but largely resilient picture. Retail sales rose sharply in March, marking the strongest monthly gain in over three years, driven in part by higher fuel prices. Even excluding this component, underlying demand remained solid. However, consumer sentiment weakened, reflecting ongoing concerns about inflation, which showed signs of re-accelerating. Business activity improved modestly in April, though rising input costs and pricing pressures suggested inflationary dynamics remain entrenched. In fixed income markets, US Treasury yields moved higher, resulting in negative returns, while corporate bonds proved relatively more resilient.

Europe

European equities declined over the week, with the STOXX Europe 600 Index falling amid heightened geopolitical tensions linked to the Middle East. Defensive sectors such as utilities and telecommunications outperformed, reflecting a more cautious investor stance. Major indices across Germany, France, Italy, and the UK all posted losses.

Economic indicators were broadly weak. German business confidence dropped to its lowest level since the pandemic, with declines across key sectors including manufacturing and construction. French consumer confidence also fell sharply, marking its steepest drop in some time. In Spain, producer prices rose notably, driven by higher energy costs.

In the UK, data was mixed. The unemployment rate declined unexpectedly, though partly due to reduced labour force participation. Retail sales exceeded expectations, supported by fuel and non-food spending. However, consumer confidence deteriorated significantly, underscoring ongoing pressure on household sentiment.

Japan

Japanese equity markets delivered mixed performance, with the Nikkei 225 reaching fresh highs, buoyed by strength in technology shares, while the broader TOPIX Index declined. Inflation data indicated a modest pickup, largely driven by rising energy costs linked to global geopolitical developments.

Monetary policy expectations remain cautious, with the Bank of Japan widely anticipated to adopt a wait-and-see approach as it balances inflation risks against growth uncertainties. Bond yields edged higher, while the yen weakened towards levels that may prompt official intervention. Authorities signalled close coordination with international counterparts in response to currency volatility.

China

Chinese mainland equities were relatively stable, consolidating earlier gains amid a lack of fresh domestic catalysts. Hong Kong markets underperformed slightly. Policymakers maintained benchmark lending rates unchanged, signalling confidence in the current economic trajectory following solid first-quarter growth.

Geopolitics remained in focus, with Chinese leadership calling for de-escalation in the Middle East and the reopening of key energy transit routes. Meanwhile, developments in the technology sector drew attention, as a domestic AI firm unveiled new models showcasing advancements in performance and efficiency.

Other Markets

Romania

Political uncertainty increased after the governing coalition fractured, pushing the administration into a minority position. This raises risks around the implementation of fiscal reforms tied to EU funding, although some legislative continuity may remain. The near-term outlook remains fluid as the government seeks to maintain stability while progressing key policy measures.

Major Company News:

Goldman Sachs has raised its Brent crude forecast to around $90 per barrel for year-end, up from $80, citing prolonged supply disruptions in the Gulf linked to ongoing Middle East tensions, signalling tighter energy markets and sustained upward pressure on oil prices.

Palantir continues to face scrutiny over its £330mn NHS data platform contract, with critics questioning costs and capability, while UK officials argue the system is vital for improving healthcare efficiency and reducing hospital backlogs.

Streaming giants including Netflix and Disney are driving a resurgence in TV advertising, with ad-supported tiers boosting revenues and projected to significantly expand, reshaping monetisation strategies and revitalising creative advertising in digital TV.

Jay Chen, a senior executive at Tokyo Electron, has left the company after it was discovered he had ties to investment vehicles backing Chinese semiconductor start-ups. The case highlights growing geopolitical sensitivities as China accelerates efforts to build a self-sufficient chip industry, intensifying pressure on foreign suppliers.

Xiaomi is rapidly scaling its electric vehicle ambitions, delivering 650,000 units and targeting European expansion, positioning itself as a serious challenger to Tesla with high-performance models and strong early demand.

Weekly Update

27th April 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.