Global markets faced a complex landscape this week as major central banks opted to maintain interest rates against a backdrop of escalating Middle Eastern tensions and volatile energy prices.

United States

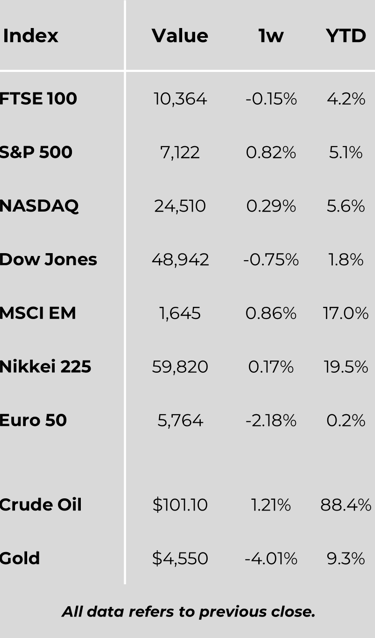

Wall Street largely shook off hawkish signals from the Federal Reserve and geopolitical uncertainty to post solid gains. The S&P 500 returned over 10% for April, its strongest monthly showing since late 2020, bolstered by robust corporate earnings. Alphabet led the "Magnificent Seven" higher on AI optimism, though Meta saw a sharp decline following plans to aggressively ramp up AI capital expenditure. On the policy front, the FOMC held rates steady, but a record number of dissents—favouring a more hawkish stance—spooked some investors. Furthermore, Jerome Powell confirmed he would remain on the Fed board even after his term as Chair concludes, citing concerns over political interference.

Europe

European indices remained broadly flat as the closure of the Strait of Hormuz and rising oil prices dampened sentiment. The ECB held its deposit rate at 2%, though officials admitted they had debated a potential hike due to "intensified" economic risks. Economic sentiment in the eurozone slumped to its lowest since 2020, with German inflation accelerating to 2.9%.

UK

In the UK, the Bank of England kept the base rate at 3.75%, warning that the inflation outlook remains "highly uncertain." Domestic retail sales figures for April were particularly bleak, hitting their lowest level since 1983.

Japan

The Nikkei 225 edged lower amidst extreme currency volatility. A sudden yen surge suggested official government intervention after the currency breached the JPY 160 level. While the Bank of Japan (BoJ) held rates at 0.75%, the 6–3 split vote indicated growing momentum for further tightening. The BoJ faces a "stagflationary" challenge, halving its growth forecast to 0.5% while raising inflation expectations to 2.8%.

China

Mainland stocks remained stable after Moody’s upgraded China’s sovereign outlook to "stable," citing fiscal resilience. Industrial profits rose by a robust 15.8% in March, driven by high-tech manufacturing. The Politburo signalled targeted support for strategic industries and AI adoption, though it notably steered clear of broad-based stimulus.

Other Markets

In a landmark shift, the UAE announced its exit from OPEC+, citing a desire to maximise production volumes - a move that highlights a growing rift with Saudi Arabia. Meanwhile, Colombia faced volatility as the central bank unexpectedly paused rate hikes amid political pressure and legal challenges to pension reforms.

Major Company News:

BP reported first-quarter profits of $3.2 billion, more than doubling last year's figures. The energy giant capitalised on volatile global oil prices, sparking renewed calls from campaigners for tougher windfall taxes.

AstraZeneca resumed its £300 million UK investment after a 2025 pause. Plans include a "lab of the future" in Macclesfield and a major expansion at its Cambridge research campus.

HSBC posted a slight decline in first-quarter pre-tax profits to $9.38 billion. Despite strong interest income, the bank was hit by higher credit losses and a £400 million UK fraud charge.

Shell reached a definitive agreement to acquire ARC Resources for $13.6 billion. The deal strengthens Shell’s shale gas position in Canada, though some analysts remain cautious regarding the premium paid.

Barclays completed its acquisition of US lender Best Egg, bolstering its digital personal loan presence. Domestically, the bank launched a new fuel cashback initiative for customers in partnership with Tesco.

Weekly Update

5th May 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.