Global markets faced headwinds this week as stubborn inflation data and surging energy costs fuelled concerns that central banks may prolong restrictive monetary policies. While the US saw rising Treasury yields and tech-led pullbacks, European markets wrestled with political instability and softer retail data. In contrast, Asian markets showed mixed resilience, with Japan adjusting to multi-decade high bond yields and China benefiting from near-term trade stability following the Trump-Xi summit. Meanwhile, historic debt restructuring plans ignited a sharp rally in Venezuelan bonds.

United States

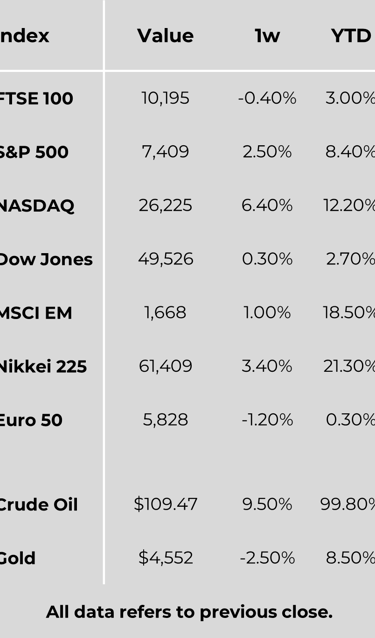

Most major US stock indexes finished lower this week. Optimism surrounding large-cap technology and artificial intelligence (AI) was ultimately outweighed by accelerating inflation, rising Treasury yields, and lingering geopolitical uncertainty. The S&P 500 hit a record high on Thursday before pulling back on Friday, with the energy sector leading gains while consumer discretionary and materials sectors declined.

US Treasuries fell as yields increased across most maturities. The benchmark 10-year US Treasury note yield climbed to approximately 4.59%, its highest level in over a year. This repricing followed hotter-than-expected inflation data; April’s Consumer Price Index (CPI) rose 3.8% year-on-year, driven largely by a 3.8% monthly surge in energy costs. Wholesale price data reinforced these persistent pressures, with the Producer Price Index (PPI) jumping 6.0% over the prior 12 months. Concurrently, retail sales rose by a modest 0.5% in April, while initial jobless claims saw a slight uptick to 211,000.

Europe

The pan-European STOXX Europe 600 Index ended the week down 0.85% as geopolitical tensions, notably stalling US-Iran peace talks, overshadowed robust quarterly corporate earnings. Germany’s DAX fell 1.59%, France’s CAC 40 declined 1.97%, and the UK’s FTSE 100 slipped 0.37%.

Macroeconomic data across the continent was mixed. Eurozone industrial production grew by a subdued 0.2% month-on-month in March. Meanwhile, French unemployment climbed to a higher-than-expected 8.1%. In Germany, investor sentiment showed signs of recovery, with the ZEW Indicator rising to -10.2, outperforming market expectations despite underlying energy worries. In the UK, political uncertainty mounted following ministerial resignations and leadership speculation within the Labour Party, pressuring both sterling and domestic equities. This political instability compounded weak consumer data, as UK retail sales fell sharply by 3.0% year-on-year in April.

Japan

Japanese equity markets delivered mixed results; the Nikkei 225 fell 2.08% due to profit-taking in semiconductor and AI-related shares, while the broader TOPIX gained 0.90%. Domestic bond yields surged, with the 10-year Japanese Government Bond (JGB) yield reaching 2.72%—its highest level since 1997—on growing expectations of an imminent Bank of Japan (BoJ) interest rate hike. In the currency markets, the yen weakened to the JPY 158 range against the US dollar, as previous official interventions had only a temporary impact.

China

Chinese equities closed lower, with the Shanghai Composite down 1.07% and Hong Kong’s Hang Seng Index falling 1.63%. Initial optimism from the Trump-Xi summit in Beijing—where both leaders signalled support for trade stability—faded later in the week. Economic data highlighted a resilient domestic landscape: April exports rose 14.1% year-on-year, and the Caixin General Services PMI climbed to 52.6. Furthermore, firmer inflation data, featuring a 2.8% year-on-year increase in the PPI, reduced market expectations for near-term monetary easing from Beijing.

Other Key Markets

Venezuela

Sovereign and PDVSA bonds rallied sharply after the government formally announced plans to restructure approximately USD 150 billion of unsustainable debt, signalling an effort to reconnect with international financial institutions.

Hungary

Newly inaugurated Prime Minister Péter Magyar pledged a market-friendly shift towards EU reconciliation and euro adoption by 2030. However, the forint experienced renewed volatility after the central bank unexpectedly lowered its foreign-currency swap rate to 5.25%.

Major Company News:

European budget airline Ryanair suspended its annual guidance and saw its shares dip 3% in Dublin, warning that the Iran conflict has inflated unhedged jet fuel prices. Despite full-year profits rising 36% to €2.4bn, rising wage bills and environmental levies are expected to pressure upcoming unit costs.

Global mining giant Anglo American has agreed to sell its Australian steelmaking coal operations to privately owned Dhilmar for $3.88bn. This closes a challenging chapter for the company after a previous sale collapsed last year following a mine explosion, which is now facing arbitration.

Global buyout firm Bain Capital has successfully closed its largest Asia-focused private equity fund after raising $10.5bn. Driven by exceptionally strong demand, external investor commitments reached $9.1bn, significantly exceeding the original $7bn target for this sixth regional fund.

Shares in Samsung Electronics rose over 4% after a South Korean court granted an injunction restricting a planned 18-day strike. The ruling mandates that normal staffing levels must be maintained to protect safety and product quality, easing fears of severe disruption to global memory chip production.

Surging oil prices have driven a 70% increase in overseas sales for Yadea, the world’s largest electric scooter manufacturer. High fuel costs have prompted the Hong Kong-listed Chinese firm to accelerate its expansion plans into the UK and Europe, specifically targeting London and Paris.

DayOne, the international spin-off of Chinese data centre operator GDS Holdings, plans a historic dual listing in Singapore and New York to raise $5bn. Set to be a major Singapore IPO, the move comes amidst heightened scrutiny over Chinese firms internationalising via the city-state.

Weekly Update

18th May 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.