Global markets ended the week on a positive footing as improving prospects for a US-Iran agreement boosted investor confidence and reduced concerns over energy supply disruptions. The resulting decline in oil prices supported risk assets globally, while continued enthusiasm surrounding artificial intelligence (AI) investment provided further momentum for technology-related shares. Equity markets generally advanced across developed markets, bond yields moved lower, and investors remained focused on the balance between easing geopolitical risks and persistent inflationary pressures that continue to influence central bank policy expectations.

United States

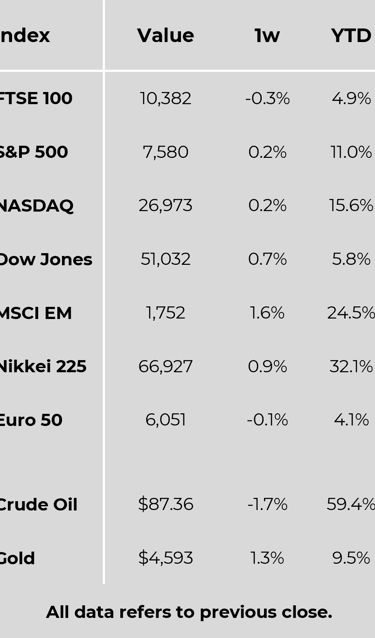

Global risk sentiment improved over the week as optimism surrounding a potential agreement between the United States and Iran supported equity markets and eased concerns over energy supply disruptions. Major US equity indices advanced, with technology shares leading gains amid continued enthusiasm for artificial intelligence (AI)-related investments. The Nasdaq Composite outperformed, while the S&P 500 and Russell 2000 also posted strong returns. Falling oil prices, driven by expectations of improved Middle East stability and a possible reopening of shipping routes through the Strait of Hormuz, provided further support for markets.

Economic data presented a mixed picture. Inflation remained elevated, with the Federal Reserve’s preferred inflation measure showing annual price growth continuing above target. While monthly inflation moderated slightly, policymakers maintained a cautious stance, signalling that inflation risks remain skewed to the upside. Elsewhere, first-quarter GDP growth was revised lower, although durable goods orders surprised positively, highlighting continued strength in manufacturing demand. US Treasury yields moved lower during the week as easing geopolitical concerns and softer energy prices supported bond markets.

Europe

European equities delivered modest gains as investors monitored developments in US-Iran negotiations and their implications for global energy markets. Germany, France and Italy recorded positive returns, while the UK market underperformed, with the FTSE 100 ending the week lower.

The European Central Bank struck a more hawkish tone, with meeting minutes suggesting growing concerns over persistent inflationary pressures, particularly those linked to energy prices. Policymakers highlighted the ongoing impact of Middle East tensions on both inflation and economic confidence. Economic data were broadly supportive, with Germany reporting a slight decline in unemployment and Italy revising first-quarter GDP growth higher. Meanwhile, European car registrations continued to rise, supported by strong demand for electric vehicles. In the UK, shop price inflation accelerated modestly, reflecting higher transportation and raw material costs.

Japan

Japanese equities rallied strongly, with the Nikkei 225 reaching fresh record highs. Investor sentiment was boosted by expectations of reduced geopolitical tensions in the Middle East, a positive development for Japan given its reliance on imported energy. Technology and semiconductor stocks led gains as investors continued to favour companies benefiting from AI-related investment trends.

Inflation data from Tokyo were softer than expected, extending a period of decelerating price growth and complicating the Bank of Japan’s policy outlook. Bond yields declined as investors reassessed inflation risks, while the yen remained broadly stable against the US dollar.

China

Chinese equity markets were mixed as stronger industrial profit data offset renewed regulatory concerns. Industrial profits accelerated in April, supported by resilient export demand and stronger earnings in energy and materials sectors. However, weakness persisted across several consumer-oriented industries, highlighting the uneven nature of China’s economic recovery.

Investor sentiment was also affected by regulatory action targeting offshore brokerage firms serving mainland investors. The crackdown weighed on Hong Kong-listed financial stocks and renewed scrutiny of cross-border investment channels.

Other Key Markets

South Korean equities benefited from strong gains in semiconductor stocks, reflecting continued confidence in the global AI and memory-chip cycle. The Bank of Korea left interest rates unchanged but adopted a more hawkish tone, signalling that future policy tightening remains under consideration.

In South Africa, the central bank raised interest rates for the first time in three years as policymakers sought to contain inflationary pressures linked to higher energy costs. While growth expectations were revised lower, an improved sovereign outlook from Moody’s provided a positive counterbalance, reflecting progress on fiscal reforms and debt management.

Major Company News:

SoftBank Group announced a major €75 billion commitment to build 5 GW of AI data center capacity in France, bolstering Europe's tech infrastructure.

US investment fund Castlelake is reportedly considering a takeover bid for EasyJet, sparking speculation that the airline could exit the struggling London stock market.

BP successfully sold a 5% stake in Australia’s massive Browse liquefied natural gas (LNG) project to South Korea's GS Energy to streamline its portfolio.

International Flavors & Fragrances (IFF) entered a binding agreement to sell its major food ingredients business to private equity firm CVC Capital Partners IX.

Morrisons is in advanced talks to sell groceries to rival supermarkets from its Myton production business, attempting to mitigate its heavy £3.1 billion debt.

Weekly Update

1st June 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.