Global equity markets delivered a mixed performance over the week as investors balanced encouraging economic data against persistent inflation concerns, geopolitical developments and shifting interest rate expectations.

United States

US equities ended the week lower, with technology stocks leading the decline. The Nasdaq Composite recorded the sharpest losses, while the S&P 500 posted its first weekly fall since March. The Dow Jones Industrial Average proved relatively resilient.

Investor enthusiasm surrounding artificial intelligence (AI) moderated as markets grappled with elevated valuations in AI-related companies, a growing pipeline of equity issuance and renewed volatility in oil prices linked to developments in the Middle East. Stronger-than-expected labour market data further weighed on sentiment by reinforcing expectations that the Federal Reserve may keep monetary policy restrictive for longer.

May's non-farm payrolls report highlighted the resilience of the US economy, with employment growth significantly exceeding forecasts. Job gains were concentrated in leisure and hospitality, healthcare and local government, while the unemployment rate remained stable at 4.3%. Additional labour market indicators were mixed, however. Job openings increased sharply and private payroll growth remained healthy, but jobless claims rose to their highest level since February and announced layoffs continued to trend upwards, with AI-related restructuring cited as a key driver.

Economic activity also remained robust. Both manufacturing and services purchasing managers' indices (PMIs) improved during May, reflecting solid demand and expanding new orders. However, inflationary pressures remained evident, with price indices across surveys continuing to signal elevated cost pressures. The Federal Reserve's Beige Book echoed this theme, reporting stronger activity across most regions alongside moderate to strong price increases.

Treasury yields moved higher over the week as stronger economic data and inflation concerns reduced expectations of near-term policy easing. Corporate bond markets also weakened, although demand for new issuance remained strong.

Europe

European markets lacked clear direction as investors assessed geopolitical developments, including potential progress in US-Iran negotiations and reports of a possible ceasefire between Israel and Lebanon. Additional uncertainty stemmed from the announcement of proposed new US tariffs on a broad range of imports.

Economic data were generally softer. Revised figures showed the eurozone economy contracted by 0.2% during the first quarter, while retail sales declined more than expected in April. France's industrial production was broadly flat, although the country's trade balance improved on stronger exports.

In the UK, new car registrations rose strongly in May, supported by continued growth in electric vehicle demand. Battery electric vehicle registrations increased sharply, highlighting the ongoing shift towards electrification.

Japan

Japanese equities delivered mixed returns as investors monitored inflation risks, energy prices and central bank policy expectations.

Comments from Bank of Japan Governor Kazuo Ueda were interpreted as increasing the likelihood of a June interest rate rise, with policymakers signalling greater concern about upside inflation risks. Wage growth exceeded expectations and real wages increased for a fourth consecutive month, although household spending remained subdued.

Meanwhile, the yen weakened further against the US dollar despite recent currency interventions, prompting renewed warnings from Japanese authorities regarding potential market action.

China

Chinese equities declined amid signs of an uneven economic recovery. Official manufacturing data suggested activity softened in May, although private-sector surveys pointed to greater resilience among smaller businesses.

Investors remained encouraged by developments within China's AI sector. Reports that Tencent is testing an AI agent within WeChat and speculation surrounding a potential fundraising round for AI start-up DeepSeek supported technology sentiment and highlighted the sector's increasing focus on commercial deployment.

Other Key Markets

Colombia

Colombian assets rallied after the first round of the presidential election delivered a stronger-than-expected showing for centre-right candidate Abelardo de la Espriella. Investors appeared to welcome the prospect of more market-friendly economic policies, supporting equities, government bonds and the peso. Higher oil prices also provided additional support, although uncertainty ahead of the run-off election is likely to keep markets sensitive to political developments.

Indonesia

Indonesia was among the weaker performers in Asia as investors responded to currency weakness, higher oil prices and growing policy uncertainty. Equities fell to four-year lows, while the rupiah weakened further, raising concerns about inflation, import costs and external financing conditions. Investors appear to be awaiting greater clarity on policy direction and currency stability before adopting a more constructive outlook on Indonesian assets.

Major Company News:

British ingredients maker Tate & Lyle has agreed to a £2.7 billion takeover by US rival Ingredion. The announcement caused the FTSE 250 company’s shares to soar.

Italian banking giant Intesa Sanpaolo launched an unsolicited €30.6 billion cash-and-share offer for Monte dei Paschi di Siena, triggering a potential bidding war with rival suitor Banco BPM.

Shares in US pharmaceutical giant Eli Lilly rose following highly positive clinical trial results for Foundayo, the company's latest weight-loss drug, further boosting its position in the obesity market.

Danish biotech firm Zealand Pharma saw its share price plunge after a high-profile trial of its experimental obesity drug saw a disappointing 20% patient dropout rate due to side effects.

Debt-laden utility company Thames Water faces crunch talks with industry regulator Ofwat this week. Speculation is mounting that a state-backed rescue deal or temporary nationalisation may be required.

Weekly Update

8th June 2026

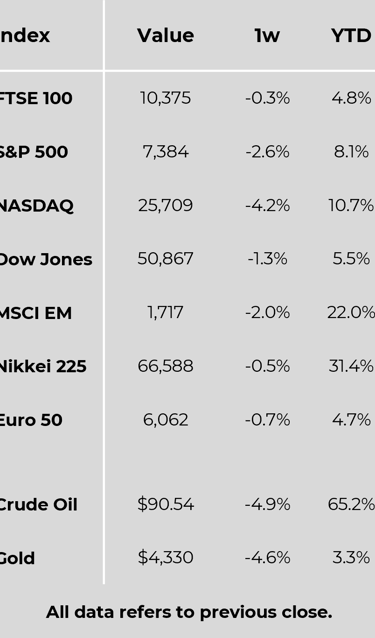

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.