Global markets have surged to record highs this morning following a landmark agreement between the United States and Iran to reopen the Strait of Hormuz. This major diplomatic breakthrough has significantly alleviated fears of a prolonged energy crisis, triggering a sharp decline in oil prices and a powerful relief rally across global equity and bond markets.

United States

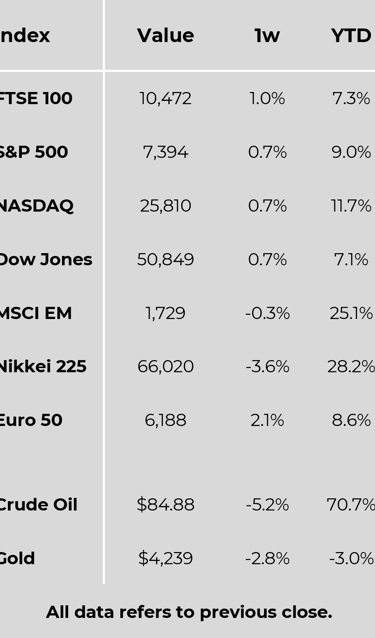

US stock futures point to a strong opening, with the S&P 500 positioned to rise 1.2%. This follows a volatile but positive week where major indices added over 0.65%. While May’s headline CPI accelerated to a three-year high of 4.2% due to historical energy pressures, core inflation showed signs of moderation. Sentiment has been significantly bolstered by Friday’s historic, blockbuster IPO of SpaceX, which closed up 19% on its debut and gained an additional 5% in Monday's pre-market trading. Consequently, Treasury yields have slid further to 4.44% as inflation anxieties ease.

Europe

The pan-European STOXX Europe 600 index climbed 1% in early trading to reach a new record high of 641.66, fully recouping its war-related losses. This follows a 1.69% gain last week, which occurred despite the European Central Bank’s interest rate hike — its first since 2023. The reopening of the shipping strait provides critical relief to the region's growth outlook, sparking a 2% surge in consumer cyclicals and industrials. Meanwhile, government bonds have rallied, with German 10-year Bund yields dropping to 2.96%.

Japan

After a volatile week where the Nikkei 225 fell 0.85% amid mounting domestic inflation and anticipation of the Bank of Japan's interest rate decision, Japanese equities soared by 5% this morning to hit a record high. The market is benefiting heavily from heavy "spillover" capital flows targeting Asian technology infrastructure. Massive gains were seen in companies critical to semiconductors, artificial intelligence, and data centres, while domestic airlines surged on expectations of lower jet fuel costs.

China

Chinese equities finished last week mixed, as robust export data contrasted with subdued domestic consumer demand. May exports jumped 19.4%, fueled by a global AI investment cycle that saw semiconductor exports double. However, the widening gap between accelerating factory-gate prices (PPI at 3.9%) and flat consumer inflation (CPI at 1.2%) reflects an uneven recovery. Strategic tensions also lingered after the US Department of Defense expanded its list of restricted Chinese technology firms.

Commodities

Reopening the Strait of Hormuz has broken the energy price shock. Brent crude plummeted 5% this morning to trade at $83 a barrel, heavily denting the short-term profit outlook for energy sector stocks.

Other Key Markets

Indonesia

Bank Indonesia delivered an unexpected, off-cycle 25 basis point rate hike to 5.5% last week to stabilise a volatile rupiah under pressure from capital outflows.

Argentina

Hard currency sovereign credit performed constructively after May headline inflation slowed to 2.1% month-on-month, leading to a credit rating upgrade to B- by S&P.

Major Company News:

SpaceX completed the largest initial public offering on record on Friday, with its shares closing up 19% on debut and gaining another 5% in Monday's pre-market trading.

Samsung Electronics saw its shares surge over 5% on Monday, acting as an Asian bellwether for the intense investor enthusiasm surrounding artificial intelligence and AI-linked tech stocks.

Alibaba Group disputed its new designation by the US Department of Defense, which added the Chinese technology champion to a restrictive procurement list over alleged ties to China's military.

Murata Manufacturing shares skyrocketed 17% on Monday as global investors rushed to maximise their portfolio exposure to Japanese businesses critical to the semiconductor, AI, and data centre industries.

Japan Airlines saw its shares surge on Monday as investors bet that reopening the Strait of Hormuz would relieve months of severe jet fuel availability concerns and flight cancellations.

Weekly Update

15th June 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.