Global equities generally advanced this week, buoyed by an ease in Middle East tensions as oil prices fell. However, central banks dominated sentiment. While the Federal Reserve held rates steady with a hawkish tilt and the Bank of England stood pat, the Bank of Japan raised borrowing costs to a 31-year high.

United States

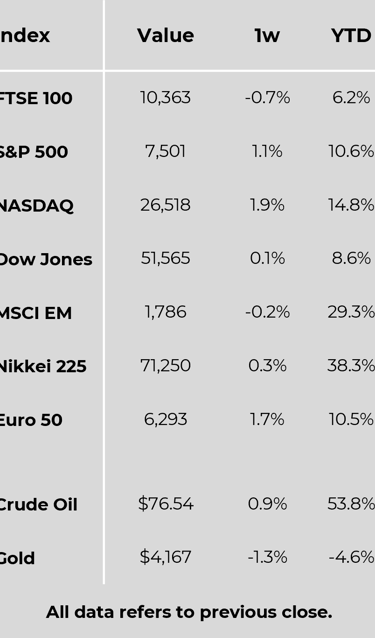

Most major US stock indexes closed higher in a holiday-shortened week, buoyed by a US-Iran memorandum of understanding to reopen the Strait of Hormuz, which lowered oil prices. The Nasdaq Composite led gains, advancing 2.43%, while the Russell 2000 and S&P 500 rose 1.21% and 0.93%, respectively. Conversely, the Federal Reserve held its target rate steady at 3.50% to 3.75%, but its Summary of Economic Projections skewed hawkish. Under new Chair Kevin Warsh, the median policymaker now forecasts modest tightening by year-end 2026, raising headline PCE inflation projections to 3.6%. This triggered a sell-off in bonds, pushing short-term Treasury yields sharply higher. Economic data proved resilient as May retail sales rose 0.9%, beating expectations. However, housing data remained mixed; housing starts plummeted 15.4%, though pending home sales rose 4.8% year on year.

Europe

The pan-European STOXX Europe 600 edged up 0.62%, supported by easing geopolitical tensions. Germany’s DAX and France’s CAC 40 gained 1.59% and 1.40%, respectively, while Italy’s FTSE MIB jumped 2.31%. Bucking the trend, the UK’s FTSE 100 slipped 0.69% as the Bank of England kept its base rate at 3.75%. UK inflation held steady at 2.8% in May, though the bank noted that Middle East price impacts remain hard to predict. Macroeconomic data across the continent was varied; the eurozone recorded an unexpected €1 billion trade deficit for April due to an expanding energy deficit. Conversely, German wholesale price inflation moderated to 5.9% in May, and the ZEW economic sentiment indicator turned positive for the first time since the outbreak of the Middle East conflict.

Japan

Japanese equities surged, with the Nikkei 225 leaping 7.62% to fresh all-time highs, driven by global artificial intelligence capital expenditure benefiting tech and semiconductor stocks. The Bank of Japan (BoJ) delivered a widely anticipated 25-basis-point hike, lifting its short-term policy rate to 1%—its highest since 1995—to counter yen weakness and inflation risks. With Governor Kazuo Ueda hospitalised, Deputy Governor Shinichi Uchida struck a hawkish tone, hinting at further normalisation. The 10-year JGB yield dipped slightly to 2.61%, while the yen weakened to JPY 160.8 against the US dollar, prompting intervention warnings. On the data front, May customs exports climbed 17.0% year on year, and April core machinery orders rebounded sharply by 8.7%.

China

Chinese mainland equities finished higher, with the CSI 300 up 3.44% and the Shanghai Composite rising 1.46%, though Hong Kong’s Hang Seng index fell 3.21%. May economic data pointed to an uneven recovery; industrial production rose 4.5% year on year on robust exports, but domestic demand floundered as retail sales contracted 0.6%. Property sector woes persisted, with investment down 16.2% for the first five months of 2026, though first-tier cities saw new-home prices rise for a third month. Meanwhile, People's Bank of China Governor Pan Gongsheng announced framework improvements, including narrow short-term interest rate corridors, prioritizing market infrastructure over aggressive stimulus.

Other Key Markets

Brazil

The central bank lowered its Selic rate by 25 basis points to 14.25%. However, policymakers struck a cautious note as May inflation unexpectedly accelerated to 4.72% year on year, stoking fiscal risk concerns.

Indonesia

Bank Indonesia raised its benchmark rate by 25 basis points to 5.75%—its third hike in a month—to defend the rupiah and combat import-driven inflation.

Major Company News:

SpaceX made a historic Nasdaq debut last week by executing the largest initial public offering in history. Strong investor demand propelled SpaceX to a staggering $1.77 trillion valuation.

Intel shares surged following news that the firm will build a US chip manufacturing alliance with Apple. This landmark Intel and Apple partnership heavily boosted domestic semiconductor outlooks.

Accenture saw its stock price plummet by 18% after reducing its full-year fiscal revenue forecast. This sudden downgrade by Accenture triggered a wider sector sell-off in technology equities.

EasyJet formally rejected a £4.7 billion non-binding acquisition proposal submitted by the US investment firm Castlelake. The easyJet board dismissed Castlelake’s 625p-per-share premium offer as highly opportunistic.

Nextpower signed a definitive €330 million cash-and-stock deal to purchase Germany’s Zimmermann PV-Steel Group. By incorporating Zimmermann PV-Steel Group, Nextpower intends to aggressively scale its European solar platform.

Weekly Update

22nd June 2026

Markets Data

This publication is intended to be Hexagon Wealth’s own commentary on markets for clients. Hexagon Wealth Limited is authorised and regulated by the Financial Conduct Authority. FCA number 483403. Hexagon Wealth Limited is registered in England and Wales under company number 04503414. Whilst Hexagon Wealth uses reasonable efforts to obtain information from sources which it believes to be reliable, it makes no representation that the information or opinions contained in this document are accurate, reliable or complete and will not be liable for any errors, nor for any actions taken in reliance thereon. Such information and opinions are subject to change without notice. We expect readers to rely on their personal views on the subject when reading the opinions expressed above and contact their financial adviser before taking any action. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice please contact your financial adviser.